Before testing this VANZEV Bull & Bear Market Fleece Blanket 60×80, I didn’t realize how much a simple piece of warmth could brighten your day. Its soft flannel fabric feels luxurious and cozy, perfect for snuggling on the couch during cold nights. I was impressed by its versatile design—great as a blanket for your sofa, bed, or even outdoor use. The variety of sizes makes it easy to find one that fits your space and needs, without sacrificing comfort or durability.

From my experience, this blanket’s durability and ease of cleaning stand out—machine washable, it stays soft without pilling or deformation. It’s an all-around practical choice that combines comfort with quality craftsmanship. So, if you want something that not only feels great but also lasts through regular use, I highly recommend giving this blanket a try. It’s like wrapping yourself in warmth that’s built to last—and your home will thank you for it.

Top Recommendation: VANZEV Bull & Bear Market Fleece Blanket 60×80

Why We Recommend It: This blanket offers superior softness with high-quality flannel, plus a versatile size range that caters to different needs. Unlike the other options—such as the extensive business plan or unrelated products—it provides genuine comfort, durability, and practicality for everyday use. Its machine washability and resistance to pilling make it a standout value.

Best place to finance a couch: Our Top 2 Picks

- VANZEV Bull & Bear Market Fleece Blanket 60×80 – Best for Comfort and Style

- How to Start a Couch Distributor Plus Business Plan – Best for Business Financing Guidance

VANZEV Bull & Bear Market Fleece Blanket 60×80

- ✓ Ultra-soft and cozy

- ✓ Versatile for home and travel

- ✓ Durable and easy to clean

- ✕ Slightly thin compared to heavy blankets

- ✕ Limited color options

| Material | High-quality flannel fabric |

| Size Options | Available in three sizes (e.g., child, adult, double) |

| Dimensions | 60×80 inches (152×203 cm) |

| Temperature Suitability | Warm and suitable for cold seasons |

| Care Instructions | Machine washable and hand washable, retains softness after cleaning |

| Intended Use | Home (sofa, bed, chair), picnic, travel |

I honestly didn’t expect a fleece blanket to feel like wrapping myself in a cloud, but this VANZEV Bull & Bear Market Fleece Blanket proved me wrong. The moment I unfolded it, I was struck by how incredibly soft and plush it felt, almost like a gentle hug.

It’s surprisingly lightweight for how warm it keeps you, which makes it perfect for those chilly evenings.

The size, at 60×80 inches, is just right—big enough to cozy up on the sofa or bed without feeling overwhelming. I used it on my couch during a rainy weekend, and it instantly transformed my lounging experience.

The high-quality flannel material is smooth and durable, holding up well after a couple of washes. I was worried about it losing softness, but it stayed just as plush as day one.

What I really appreciate is its versatility. It’s not just for home; I threw it in my backpack for a picnic, and it doubled as a warm mat on the grass.

It’s lightweight enough to carry around but still provides serious warmth. Plus, it’s easy to clean—just toss it in the washing machine, and it comes out soft and intact, no shedding or deformation.

If you’re thinking about gifting something thoughtful, this blanket hits the mark. It’s a cozy, practical gift for friends or family, perfect for birthdays or holidays.

Honestly, I’ve been using it daily, and I keep discovering new ways it makes my chill time comfier.

How to Start a Couch Distributor Plus Business Plan

- ✓ Comprehensive business plan

- ✓ Extensive lender directory

- ✓ Easy-to-use financial model

- ✕ Digital delivery only

- ✕ Might need industry background

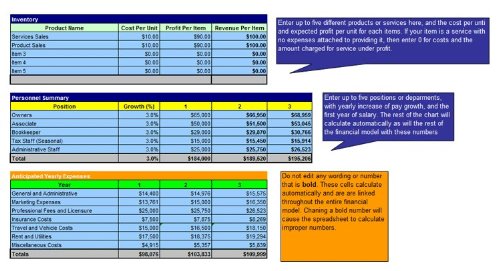

| Content Format | MS Word document for business plan, including industry research |

| Financial Model | Easy-to-use MS Excel 3-year financial projection tool |

| Additional Resources | Includes SBA approved lender directory with 425+ entries |

| Delivery Method | Delivered via CD-ROM |

| Shipping Policy | Same day shipping if ordered before 5PM EST |

| Business Planning | 9-chapter comprehensive business plan guide |

You’ve probably stared at that empty space in your living room, wondering how to turn your passion for couches into a real business without drowning in confusing guides or outdated info. I felt the same way until I came across this comprehensive starting kit for a Couch Distributor business.

It’s like having a seasoned mentor holding your hand through every step.

The first thing that caught my eye was the 9-chapter business plan in MS Word. It’s detailed but easy to follow, with real industry research included.

I appreciated how it breaks down the process into manageable chunks, making the big dream of owning a couch business seem less overwhelming.

The SBA-approved lender directory is a game-changer. With 425+ options, I could quickly identify potential financing sources without endless searching.

Plus, the same-day shipping meant I had everything I needed in my hands fast, even if I ordered late in the day.

The financial model in Excel is surprisingly user-friendly. I was able to input my numbers and get a clear picture of my three-year projections.

It takes the guesswork out of planning, which is exactly what I needed to feel confident about moving forward.

Overall, this package simplifies what can feel like a complicated process. It combines industry research, practical tools, and expert guidance in one accessible package.

If you’re serious about starting a couch business, this is a solid starting point.

What Are the Best Financing Options for Buying a Couch?

The best financing options for buying a couch include personal loans, credit cards, financing through retailers, and rent-to-own agreements.

- Personal Loans

- Credit Cards

- Retailer Financing

- Rent-to-Own Agreements

When exploring these options, each offers different benefits and potential drawbacks.

-

Personal Loans: Personal loans provide a fixed amount of money that you repay in monthly installments. This option typically has lower interest rates compared to credit cards, making it more affordable in the long run. According to Experian data, average personal loan rates range from 6% to 36%. For example, if you secured a $1,000 personal loan at a 10% interest rate over three years, your monthly payment would be approximately $32.

-

Credit Cards: Credit cards allow you to purchase a couch and pay it off over time. Many credit cards offer promotional terms such as 0% APR for an introductory period. However, rates can significantly increase after the promotional period. For instance, if you use a credit card with a 20% interest rate and do not pay off the balance during the promotional period, you might end up paying considerably more. According to the Federal Reserve, the average credit card interest rate is around 16%.

-

Retailer Financing: Many furniture retailers offer in-house financing options that allow you to pay for your couch over time. These plans sometimes come with interest-free periods, but they may also carry high annual percentage rates (APR) after the promotional period ends. A survey by Consumer Reports found that around 30% of consumers regret financing through retailers due to hidden fees or high interest rates.

-

Rent-to-Own Agreements: Rent-to-own allows you to rent a couch with the option to buy it later. This option can be appealing for those with bad credit or those who do not want to commit to a purchase initially. However, overall costs can be high. A research study by the National Consumer Law Center indicates that consumers can end up paying two to three times the retail price through rent-to-own agreements.

Each of these financing options presents distinct advantages and disadvantages, which consumers should carefully assess based on their financial situation and preferences.

How Can You Find No-Credit-Check Financing for Couch Purchases?

You can find no-credit-check financing for couch purchases through various methods, including retail financing options, rent-to-own agreements, and online lenders specializing in bad credit.

Retail financing options often include in-store promotions providing easy payment plans. Many furniture stores offer financing directly to customers that allows for quick approvals without credit checks, focusing instead on income and employment verification. For example, brands like Ashley Furniture and Raymour & Flanigan frequently provide such offers to encourage purchases. Additionally, some retailers partner with third-party financing companies to provide flexible payment solutions.

Rent-to-own agreements allow customers to take home furniture and pay in installments. This option typically does not require a credit check, and you can return the item if you choose not to purchase it outright. Companies like Rent-A-Center and Aaron’s offer this service, making it accessible to those needing immediate furniture without substantial upfront costs.

Online lenders that specialize in bad credit provide another alternative. They often offer personal loans with no credit check required. These loans can be used to purchase a couch or finance larger furniture pieces. Companies such as Upstart and Avant focus on alternative data for credit evaluation, allowing individuals with limited or poor credit histories to qualify.

Lastly, community financial institutions or local credit unions may provide financing options with lower eligibility requirements. They often have programs designed to assist individuals with poor credit for necessary purchases, making them a viable choice for sofa financing.

These methods can provide financing solutions without the burden of a credit check, enabling individuals to purchase necessary furniture affordably and conveniently.

What Flexible Payment Options Are Available for Couch Financing?

The flexible payment options available for couch financing typically include financing plans, leasing agreements, and layaway programs.

- Financing Plans

- Leasing Agreements

- Layaway Programs

- Buy Now, Pay Later Services

- Zero-Interest Financing

- Deferred Payment Options

Understanding these options enables consumers to choose the best solution for their financial needs.

-

Financing Plans: Financing plans allow customers to pay for their couch over time through monthly installments. These plans often come with interest rates, which can vary. Some retailers offer no-interest plans as promotional deals. For example, many stores provide 12 or 24-month financing options, where customers can pay off their purchases within the promotion period without incurring interest.

-

Leasing Agreements: Leasing agreements involve renting the couch for a specified period with the option to purchase at the end. This arrangement allows consumers to enjoy the furniture immediately without a large upfront cost. Monthly payments are usually lower than financing options, but consumers do not own the furniture until the final payment is made.

-

Layaway Programs: Layaway programs allow customers to reserve a couch by making smaller payments over time, which secures the item until it is fully paid for. Customers typically pay a deposit to hold the item, and payments continue until the total cost is covered. The couch is then delivered or picked up at the end of the payment period.

-

Buy Now, Pay Later Services: Buy now, pay later services are increasingly popular. These programs enable customers to acquire a couch and split the payment into manageable installments. This method often includes last-minute sign-up incentives but can carry late fees if payments are missed.

-

Zero-Interest Financing: Zero-interest financing plans provide consumers the opportunity to finance their couches without accruing interest. This option often requires customers to pay off the balance within a specified time frame, typically ranging from six months to two years. Retailers may offer this incentive during promotional events to attract buyers.

-

Deferred Payment Options: Deferred payment options allow consumers to delay their first payment for a specific period. This gives customers a grace period to start using the couch before beginning payments. It’s a helpful option for those anticipating an increase in their budget shortly.

These flexible options cater to different financial situations and preferences, allowing consumers to choose the method that best suits their needs while managing the cost of their new couch.

What Are the Advantages of Financing a Couch Instead of Paying in Full?

Financing a couch offers several advantages compared to paying in full. It allows consumers to manage their budget more effectively while providing access to higher-end furniture.

- Improved Cash Flow Management

- Immediate Enjoyment of the Product

- Flexible Payment Options

- Potential for Building Credit

- Access to Promotions or Discount Offers

- Financial Safety During Emergencies

- Higher Cost Items Become Affordable

- Interest-Free Financing Options

The benefits of financing can vary greatly depending on individual circumstances and financial situations, which leads to differing opinions on whether it is the best choice.

-

Improved Cash Flow Management:

Improved cash flow management occurs when consumers split the cost of a couch into smaller payments. This allows them to keep a larger portion of their savings intact. For instance, instead of spending $1,000 upfront, a customer might finance the couch for $100 a month for ten months. This method can help allocate funds for other necessary expenses such as bills or groceries. -

Immediate Enjoyment of the Product:

Immediate enjoyment of the product means that consumers can start using their new couch right away while paying for it later. This benefit enhances comfort in the home without waiting to save enough money. For example, a family can host gatherings and enjoy their living space immediately after purchase. -

Flexible Payment Options:

Flexible payment options provide various choices to consumers regarding their financing terms. This can include longer repayment periods or different payment schedules, allowing customers to select what best fits their financial situation. Retailers may offer monthly, bi-weekly, or even weekly payment options, catering to diverse income schedules. -

Potential for Building Credit:

Potential for building credit refers to the positive impact financing can have on a consumer’s credit score. By making timely payments on their couch, consumers demonstrate responsible borrowing, which can lead to improved credit ratings. According to Experian, responsible credit use can enhance one’s credit score by at least 20-30 points over time. -

Access to Promotions or Discount Offers:

Access to promotions or discount offers can make financing an attractive choice. Many retailers provide special financing deals that include promotional periods with no interest. For instance, a consumer may finance a couch and not pay interest for 12 months if they pay off the balance within that period. This can lead to considerable savings. -

Financial Safety During Emergencies:

Financial safety during emergencies allows consumers to maintain a financial cushion when unexpected expenses arise. Financing a couch keeps a consumer’s savings intact for emergencies, reducing stress in case of medical bills or car repairs. For example, someone may have $2,000 saved and choose to finance a couch for $800, preserving cash for urgent needs. -

Higher Cost Items Become Affordable:

Higher cost items become affordable when financing spreads the payment across time. This option permits consumers to purchase items they would otherwise find too expensive. A luxury sofa priced at $1,800 may seem daunting, but financing it can make it reasonable with monthly payments of $150. -

Interest-Free Financing Options:

Interest-free financing options enable consumers to pay for furniture without incurring extra costs. Many retailers offer interest-free periods, which can save customers money compared to traditional loans. For instance, a retailer might offer a 0% interest rate for the first 12 months on a couch purchase, allowing the consumer to pay off the balance at no extra cost.

What Factors Should You Consider Before Selecting a Couch Financing Plan?

Considering a couch financing plan requires careful evaluation of several factors.

- Interest rates

- Loan terms

- Monthly payment amounts

- Total cost of financing

- Credit score requirements

- Down payment requirements

- Fees and penalties

- Retailer reputation

- Flexibility in repayment options

These factors play a critical role in shaping whether the financing plan suits your financial situation and needs.

-

Interest Rates: Interest rates are the cost of borrowing money, expressed as a percentage. Higher rates increase the overall cost of the couch. According to Experian, the average interest rate for loans can vary significantly based on your credit score and the lender, influencing how much you pay in total.

-

Loan Terms: Loan terms refer to the duration for which you agree to repay the loan. Longer terms reduce monthly payments but increase total interest paid. A study by the Consumer Financial Protection Bureau indicates that shorter terms often yield lower interest costs over the loan’s life.

-

Monthly Payment Amounts: Monthly payment amounts determine your financial commitment each month. These amounts depend on the total loan, interest rates, and loan terms. Ensuring payments fit your budget is crucial to avoid default.

-

Total Cost of Financing: The total cost includes the principal and all interest payments over the life of the loan. For example, financing a $1,000 couch at 10% interest over 24 months could cost over $1,100, emphasizing the need for clear calculation before agreeing to a plan.

-

Credit Score Requirements: Many lenders have specific credit score thresholds. A better score can lead to lower interest rates. The Fair Isaac Corporation states that borrowers with higher credit scores typically receive more favorable loan terms, thus saving money in the long run.

-

Down Payment Requirements: Down payment refers to the upfront payment you need to make when financing. A larger down payment can lower the loan principal and reduce monthly payments. This can also demonstrate financial responsibility to lenders.

-

Fees and Penalties: Fees may include origination fees or prepayment penalties. Understanding these potential costs is essential, as they can add to the total cost of financing. Always read the financing agreement carefully for hidden costs.

-

Retailer Reputation: The reputation of the retailer impacts customer experiences with financing plans. Researching customer reviews and satisfaction ratings can provide insight into service quality and potential issues with the financing process.

-

Flexibility in Repayment Options: Flexible repayment options allow borrowers to adjust their payments in times of financial strain. Lenders offering options like skipping a payment or adjusting down payment amounts can ease financial burdens.

Evaluating these factors offers a comprehensive understanding of how to choose the right couch financing plan tailored to your needs.

Which Retailers Provide Couch Financing with No-Credit-Check Options?

Many retailers offer couch financing options without requiring a credit check.

- Ashley HomeStore

- Rent-A-Center

- Wayfair

- Bob’s Discount Furniture

- American Signature Furniture

- Aarons

- Living Spaces

- Furniture Row

Retailers provide diverse financing options. Each retailer has unique policies and terms that could impact potential customers.

-

Ashley HomeStore:

Ashley HomeStore offers financing through a lease-to-own program, which allows customers to take furniture home immediately and pay in installments. The store does not require a credit check for this option. Customers can enjoy flexible repayment terms. -

Rent-A-Center:

Rent-A-Center provides no-credit-check financing for furniture, electronics, and appliances. Customers can choose from flexible payment schedules, which can be weekly or monthly. This option allows customers to rent items and own them after fulfilling the payment commitments. -

Wayfair:

Wayfair works with third-party financing partners that may offer no-credit-check options. Customers can apply for financing through these partners directly on Wayfair’s website. The store also provides flexible payment plans tailored to the customer’s financial situation. -

Bob’s Discount Furniture:

Bob’s offers a financing program featuring zero-interest plans for customers with approved credit. Although a credit check may be required for some options, Bob’s often promotes options that do not depend solely on credit scores, particularly through regional promotions. -

American Signature Furniture:

American Signature Furniture provides no-credit-check financing through a partnership with various financial organizations. This allows customers with bad or no credit histories to access financing. Their terms typically include flexible payment options. -

Aarons:

Aarons is a rental and lease-to-own retailer that does not require a credit check. Customers can take furniture home right away and make flexible weekly or monthly payments. Aarons promotes ownership through its lease agreements. -

Living Spaces:

Living Spaces offers multiple financing options, including programs that do not require a credit check. Customers can apply for financing through their website. They provide promotional offers such as deferred payments or low-interest plans. -

Furniture Row:

Furniture Row provides no-credit-check financing options through its In-House Credit program. This option allows customers to own their furniture while spreading the payment over time without rigorous credit evaluations.

These retailers cater to various needs and preferences. Options range from rent-to-own models to flexible payment plans that can enhance accessibility to furniture.

What Alternative Financing Solutions Can You Explore for Couch Purchases?

Couch purchases can be financed through various alternative financing solutions. These options allow consumers to obtain their desired furniture without immediate full payment.

- Buy Now, Pay Later Services

- Retailer Financing Programs

- Credit Cards with Promotional Offers

- Personal Loans

- Lease-to-Own Options

- Peer-to-Peer Lending

- No Interest Payment Plans

These financing solutions offer different structures and benefits, catering to a range of financial circumstances. Each option may come with its own advantages and potential drawbacks, allowing consumers to choose based on their specific needs.

-

Buy Now, Pay Later Services:

Buy Now, Pay Later services enable consumers to make purchases and pay for them in installments over time. Companies like Afterpay and Klarna offer these services. According to a report by McKinsey & Company (2021), this financing option has grown in popularity, appealing to younger consumers seeking flexible payment solutions. For example, if an individual wishes to buy a couch costing $800, they might choose to pay in four installments of $200 every two weeks. -

Retailer Financing Programs:

Retailers often provide their own financing programs, allowing customers to apply for credit directly at the point of sale. Many furniture stores, such as Ashley HomeStore, offer special financing terms, including deferred interest promotions. A study by the National Retail Federation in 2022 found that these promotions can significantly increase sales, as they attract customers who prefer to make payments over time. However, consumers should be cautious of the fine print and potential high-interest rates after promotional periods. -

Credit Cards with Promotional Offers:

Many credit cards offer promotional periods with no interest on purchases made during a specified timeframe. For example, consumers can find cards that offer no interest for the first 12 months on purchases above a certain amount. According to CreditCards.com, about 36% of cardholders have used promotional offers for large purchases like furniture. This option allows cost-effective financing if consumers can pay off the balance within the promotional period. -

Personal Loans:

Personal loans can be obtained from banks or credit unions and used for various purchases, including furniture. These loans typically have fixed interest rates and repayment schedules. According to Experian (2023), individuals may prefer personal loans for larger amounts or long-term financing. For instance, a borrower might take out a $1,500 personal loan to buy a couch and pay it back over three years. -

Lease-to-Own Options:

Lease-to-Own programs allow consumers to rent furniture with the option to purchase it later. Retailers like Rent-A-Center and Aaron’s provide this service. This model is popular among consumers seeking immediate access to furniture without upfront costs. According to a Consumer Financial Protection Bureau report (2021), lease-to-own arrangements can be more expensive in the long run, as fees can add up quickly if the consumer ultimately decides to purchase the item. -

Peer-to-Peer Lending:

Peer-to-peer lending platforms, such as LendingClub and Prosper, allow consumers to borrow money from individual investors instead of traditional financial institutions. This option can offer competitive interest rates based on the borrower’s creditworthiness. A study by the Harvard Business Review (2020) highlighted the growing trend of using peer-to-peer lending as a flexible solution for personal expenses, including furniture purchases. -

No Interest Payment Plans:

Some retailers offer no-interest payment plans for a set period, encouraging consumers to make purchases without immediate interest charges. Similar to promotional credit cards, these plans allow consumers to spread payments over several months. According to the American Furniture Association, these plans can lead to higher sales, particularly among consumers who prefer zero-interest financing options. They can be an excellent choice for those who can commit to making timely payments.